|

|

Economic valuation of ecosystem servicesAquatic ecosystems (wetlands) provide a wide range of ecosystem services which are valued by beneficiaries. Sometimes it can be useful to have an estimate of the monetary value of ecosystem services to assist in decision making. This page discusses various methods of valuing ecosystem services, and some economic analysis tools that use these values.

Quick facts

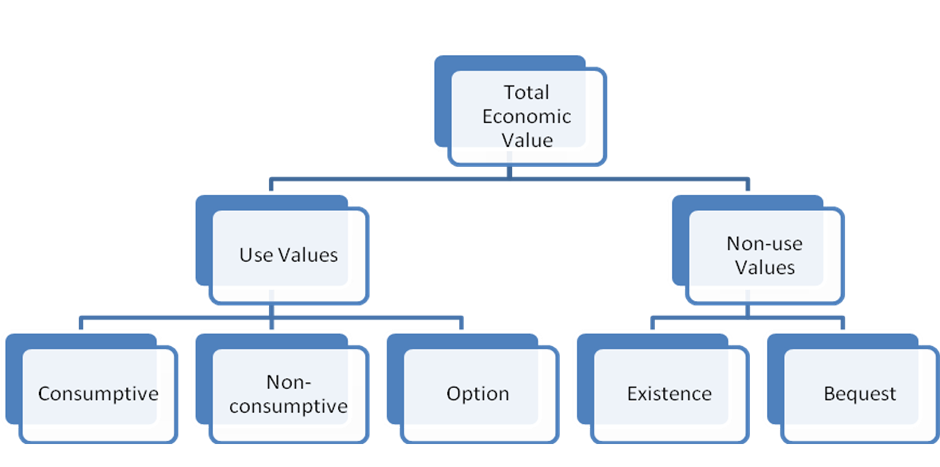

Economists often use Total Economic Value to categorise environmental goods or services. The Total Economic Value is generated from an ecosystem as a result of both use of ecosystem services and non-use values (Figure 1). The use value can be due to direct use (i.e. food, recreational activities) and indirect use (i.e. flood mitigation, supporting fish population) of the ecosystem. Direct use values can be extractive/consumptive (e.g. food) or non-extractive/non-consumptive (e.g. tourism). Humans may also value having the option to use a service in the future. Non-use values relate to the benefits humans derive from knowing that an environmental good or service simply exists, or is available for use by future generations.

It is important to note that the Total Economic Value framework is anthropocentric and focuses on the benefits humans get from nature. Many cultures, such as the First Nations people of Australia, have a wider value framework that see humans as interconnected with nature and include responsibilities to protect Country. Economic valuationIt can be useful to have monetary estimate of the Total Economic Value of an ecosystem. For example, decision making tools such as cost-benefit analysis and cost-effectiveness analysis use monetary values as inputs. This allows for the importance of all aspects of the value, both use and non-use, to be objectively considered. The value for different ecosystem services can be estimated based on market-based valuation method and non-market valuation methods. Market based valuationFor some goods and services (such as food, fish, water), the competitive market price can be considered to estimate the total value (Quantity x Market price)[15]. This is the most easily quantifiable valuation and commonly used and understood. Market failure is a economic term that refers to a situation where a market does not allocate resources efficiently[9]. There are various reasons for market failure and for environmental issues these primarily relate to the characteristics of some goods and services, and the availability of information. Non-market based valuationFor other goods and services no market price exists and non-market valuation is required. The methods for non-market valuation are underpinned by many assumptions that require additional processes to perform and can be difficult to explain. Non-market valuation of ecosystem servicesThere are two broad categories of non-market valuation – Revealed preference methods and Stated preference methods. Revealed preference methodsNon-extractive use values can be indirectly estimated through revealed preference methods. Revealed preference methods observe the behaviour of people through their market transactions and choices to assess their values of different goods and services[2]. The most common are travel cost and hedonic price methods. The travel cost method considers people’s visitation to an area (such as a wetland) which is dependent on its tangible (such as fish) and non-tangible (such as bird watching) uses and the time and expenses incurred for each visit that represent the visitors’ willingness to pay[13]. This willingness to pay is taken to represent the value the visitor holds for the area. There are two travel cost methods, individual travel cost (individual expenses for visiting) or zonal travel cost method (considering average visitors from different zones). The hedonic pricing method analyses property transactions to estimate the non-tangible benefits such as a nice view of wetland. A property can be valued based on a number of characteristics, which includes surrounding characteristics such as green space or views the surrounding landscapes. Considering the heterogeneity of properties, a value for each characteristic can be assessed[8][7]. Stated preference methodsStated preference methods directly elicit values from the public for existing ecosystem services as well as potential changes to ecosystem services using specially designed methods[1]. These method presents hypothetical scenarios in surveys with different combinations of characteristics of a natural entity. Respondents can then be asked to rank or choose their best (worst in some cases) preferences. A monetary estimate of various characteristics of the ecosystem services are then derived from the responses. Discrete choice experiment method, contingent valuation method and best-worst scaling are some common stated preference methods used in ecosystem valuation. A discrete choice experiment is commonly used and involves constructing different hypothetical scenarios of ecosystem improvement to allow respondents to compare with the status quo situation. Based on their bids, the value for different ecosystem services can be assessed. In the contingent valuation method a single choice is offered to compare with the status quo option and respondents are asked to bid the maximum (or minimum) value (or in different method of payment such as willing to increase tax) they are willing to pay. Best-worst scaling analysis helps in comparing the importance of different ecosystem services. In some situations, cost-based methods (abatement cost, restoration cost or replacement cost) can used to value an ecosystem. For instance, erosion can be prevented using an engineering construction instead of wetland. The cost of the construction can be seen to be the replacement value for the wetland – the wetland is worth at least as much as the replacement would cost.

Benefit TransferUndertaking non-market valuation studies is often time-consuming and expensive as it requires technical expertise and often field work. However, in some cases it may be appropriate to “transfer” the findings from completed non-market valuation studies which have been conducted in another site. Benefit transfer is assisted by databases of environmental valuation studies, such as the Canadian Government’s EVRI. Using information from other studies can help give an idea of indicative values for ecosystem goods and services. However, if this information is to be used for decision making an economist should be consulted, as there are many considerations to be taken into account when carrying out the transfer (such as the similarities between the characteristics of the original study and the proposed application). Economic analysis toolsEconomic analysis tools can help decision makers determine if intervention is necessary and assess a range of intervention options, including benefits to society and maximising benefits. The most commonly used appraisal tools in Australia are cost-benefit analysis, cost-effectiveness analysis and multi-criteria analysis. Cost-benefit analysis is widely used for analysing the economic, social, environmental and cultural values of government policies[3],[10],[12]. The method helps decision makers understand the overall welfare gains or losses to society that accrue from a policy proposal and the relative costs and benefits of potential options. A cost-benefit analysis compares the total costs and benefits of different policy options against the status quo. If the benefits are greater than the costs the policy represents an overall benefit to society. Preferably all values should be expressed in monetary terms – generated by the valuation methods described above – so that they can easily be compared. However, non-market valuation is not always a good indicator of the true cost or benefit to society due to reasons such as technical challenges, problems with the process used or inappropriateness due to factors such as cultural sensitivity. When monetisation is not possible or practical it is important that the values are described in a qualitative manner. The process of systematically gathering information on the relative costs and benefits of different policy options, even if this information is only described qualitatively, helps improve the decision making process. Cost-effectiveness analysis chooses an outcome and compares the costs of reaching that outcome. For example, a government has committed to meeting a water quality target, and the costs of various options for meeting that target are compared. This approach is most suitable when the options have similar rates of effectiveness[10]. The main limitation to cost-effectiveness analysis is that it assumes that the outcome is desirable and does not determine overall ecosystem service outcomes and costs. There is more information on assessing costs and cost effectiveness for treatment systems for pollutant removal. Multi-criteria analysis is a decision making tool that involves choosing selection criteria, assigning weights and scoring the options against the criteria. The options are then ranked. This method assists with comparing options on many different aspects without the use of monetary valuations. As with cost-effectiveness analysis, however, multi-criteria analysis cannot say if overall benefits outweigh costs. It can also be difficult to replicate as the scoring process may be dependent on the judgements of panellists involved weighting and scoring the options. Environmental economic accountingThere are many different environmental economic accounting (sometimes referred to as natural capital accounting) systems available for landholders and societies to measure aspects of natural capital. At a national level, having a system of formal environmental economic accounting can complement traditional national accounts such as Gross Domestic Product (GDP). Increasing the visibility of natural stocks and flows may help ameliorate the risk of national accounts ignoring the value of nature to humans[16]. The United Nations Statistical Commission has adopted a formal method for assessing national natural capital called the System of Environmental Economic Accounting (SEEA). Because these accounts are designed to complement other national accounts, they use exchange values which are the prices the goods or services attract in the marketplace, or make estimates of what these value might be in the cases where markets do not exist[11]. As a result, SEEA will sometimes have much lower values for the environment than the welfare methods discussed above[6]. As well as SEEA, there is the System of Environmental Economic Accounting - Ecosystem Accounting (SEEA EA), which is a framework for organising biophysical information about ecosystems, measuring ecosystem services, tracking changes in ecosystem extent and condition, valuing ecosystem services and assets and linking this information to measures of economic and human activity[17]. SEEA EA consists of physical accounts measuring ecosystem extent and ecosystem condition to form stock accounts, and then measures ecosystem services, or flows, associated with those stocks. SEEA EA aims to measure these services monetarily, though this is not necessary for the accounts to still be useful.

As SEEA EA is an accounting measure it is focused on the use values of nature (discussed above)[17]. This means it will only provide a limited view of the value of nature – for example, the large non-use values people hold for the Great Barrier Reef would not be captured in a SEEA EA natural capital account. Instead, the asset would be seen to generate services such as seafood, recreational services and perhaps local benefits such as coastal defence. The UN however has provided for the possibility of proxy measures to capture data related to non-use values[17][14]. At regional and local levels or for corporate uses it might not be as important to follow strict SEEA guidelines as no comparison to national accounts will be made[5][4]. This would allow for the possibility of mixing exchange and welfare values. Cost-based methods such as replacement value might also be appropriate. Pages under this sectionReferences

Last updated: 30 April 2024 This page should be cited as: Department of Environment, Science and Innovation, Queensland (2024) Economic valuation of ecosystem services, WetlandInfo website, accessed 8 May 2025. Available at: https://wetlandinfo.des.qld.gov.au/wetlands/management/wetland-values/economic-valuation/ |

Site footer

— Department of the Environment, Tourism, Science and Innovation

— Department of the Environment, Tourism, Science and Innovation